You’ve probably heard about the Federal Reserve in the news, especially when interest rates change or the economy seems shaky. But what exactly does the Fed do, and why should you care? Let’s break down this powerful but often misunderstood institution in plain English.

Why We Need the Fed

Imagine if there was no one keeping an eye on the banking system. That’s exactly what America looked like before 1913, and it wasn’t pretty. The economy swung wildly between good times and terrible crashes. Banks failed regularly, and people lost their life savings overnight.

Things got so bad during the Panic of 1907 that the country had to rely on a wealthy banker named J.P. Morgan to bail out the financial system. When unemployment doubled and the economy shrank by 10%, Americans decided enough was enough. Congress created the Federal Reserve in 1913 to prevent these kinds of disasters.

Today, the Fed has grown into one of the most important institutions in the country, affecting everything from your job prospects to how much you pay in interest on a car loan.

What Does the Fed Actually Do?

Think of the Fed as having two main jobs that sometimes pull in opposite directions. First, it tries to keep prices stable so your money doesn’t lose value to inflation. Second, it works to make sure as many Americans as possible can find jobs. Balancing these two goals is the Fed’s constant challenge.

To do this, the Fed raises and lowers interest rates. When prices are rising too fast (inflation), the Fed raises rates to cool things down. When unemployment is climbing, it lowers rates to encourage businesses to borrow, invest, and hire more workers.

Who’s Running the Show?

The Federal Reserve isn’t just one office in Washington. It’s actually a network of institutions working together.

The Federal Open Market Committee is the group that meets regularly to decide whether interest rates should go up, down, or stay the same. These decisions affect everything from credit card rates to how much businesses pay to borrow money.

The Board of Governors includes seven people appointed by the president to 14-year terms. These long terms are intentional—they’re designed to keep the Fed focused on what’s best for the economy long-term, not what’s popular with politicians right now.

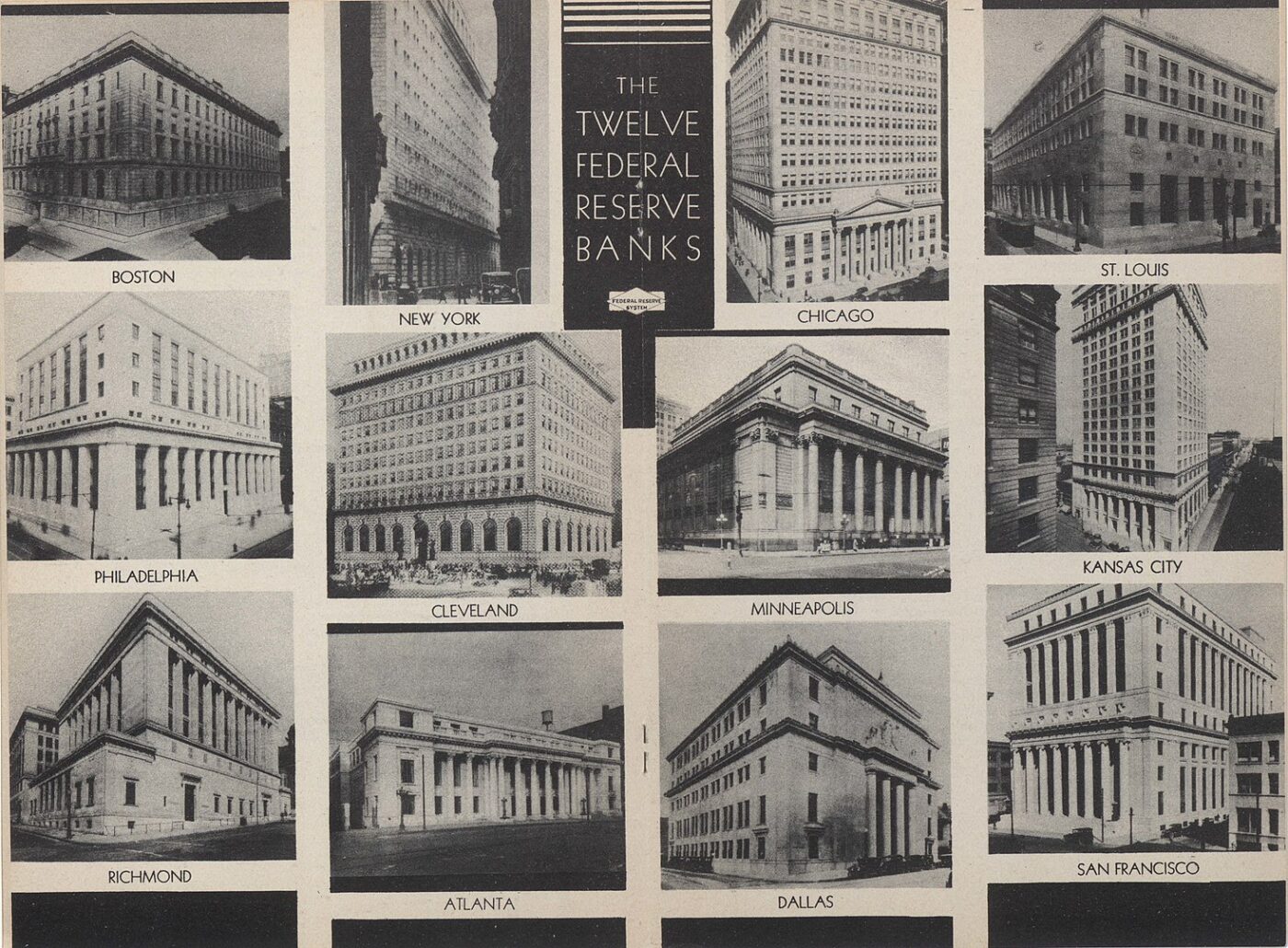

Twelve Regional Reserve Banks are scattered across the country, from Boston to San Francisco. They serve as “banks for banks,” helping the financial system run smoothly. They also conduct research on the economy. You might have used the St. Louis Fed’s FRED database, which offers free access to hundreds of thousands of economic statistics.

The Fed Gets Creative During Crises

When the financial crisis hit in 2008, the Fed didn’t just stick to its usual playbook. It tried new approaches, including buying up mortgage-related investments to support the housing market. These creative solutions helped restore confidence and steady the economy.

After that crisis, the Fed took on additional responsibilities. It now stress-tests major banks annually to make sure they could survive another downturn and watches more carefully for warning signs of financial trouble brewing.

Busting a Big Myth About Mortgage Rates

Here’s something that confuses a lot of people: when the Fed cuts its main interest rate, mortgage rates don’t automatically fall. In fact, since the Fed started cutting rates in September 2024, average 30-year mortgage rates actually went up—from about 6.2% to 6.7%.

Why? The Fed only directly controls one rate: the federal funds rate, which is what banks charge each other for overnight loans. This influences things like credit card rates and auto loans. But mortgage rates depend more on where people think the economy and inflation are headed over the long term.

Why Fed Independence Matters to You

You might have seen headlines about President Trump or other politicians trying to influence Fed decisions. There’s a good reason the Fed is designed to resist this pressure.

Politicians love the idea of lower interest rates because they can boost the economy and create jobs in the short term—which means more votes. Senator Elizabeth Warren, for example, publicly pushed the Fed to cut rates faster in 2024. But cutting rates too early can backfire badly.

Back in the early 1970s, President Nixon pressured the Fed to keep rates low before his reelection. Many economists believe this helped cause the terrible inflation of the 1970s, when prices spiraled out of control and people’s savings lost value rapidly.

The Fed’s independence—protected by long terms for its leaders, self-funding, and a decentralized structure—allows it to make tough decisions that benefit the economy over time, even when those decisions are unpopular in the moment.

The Fed Isn’t Perfect

Even with armies of economists and mountains of data, the Fed has to make decisions based on incomplete information. Economic reports often get revised weeks or months later, which means everyone—including the Fed—is working with an imperfect picture of what’s actually happening.

That’s why you’ll sometimes see the Fed make decisions that seem surprising or change course unexpectedly. They’re doing their best with the information available, knowing that waiting for perfect data isn’t an option when the economy is moving in real time.

What This Means for You

The next time you hear about the Fed in the news, you’ll understand what’s really at stake. Whether you’re thinking about buying a home, worried about your job security, or just trying to make sense of why prices keep rising, the Fed’s decisions play a role.

Political pressure on the Fed will always make headlines, but what matters most is whether the Fed can stay focused on its job: keeping the economy stable and Americans employed. Understanding how it works—and why it’s designed the way it is—helps you see past the noise and focus on what really affects your wallet and your future.

Marc Goldstein, our Finance Editor, is a nationally known Financial Educator and Retirement Wealth Specialist, who helps people protect and pass on their wealth.

https://www.mgoldsteinassoc.com/